Deductible

Choose the deductible that fits your risk.

The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation.

- ✓CHF 300 to CHF 2,500

- ✓Personal risk

- ✓Premium optimization

Which deductible fits in Switzerland? PrimAI helps check risk, expected health costs and official premiums in the free app.

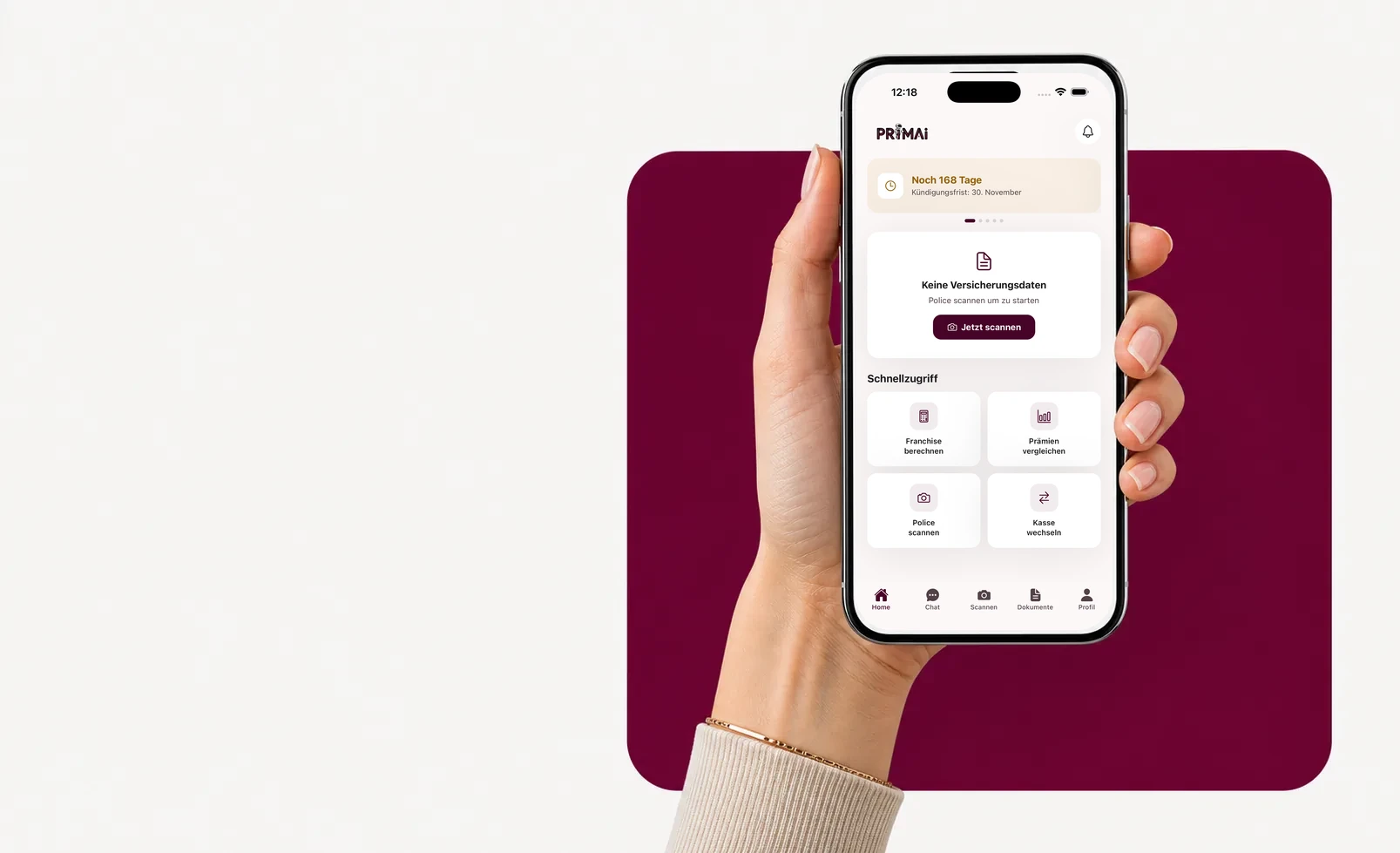

PrimAI app

Turn your policy into a clear app task.

Scan your policy, check official FOPH premiums, keep the deadline in view and prepare the right document — neutral, free and without commission.

Guide

What is the deductible?

The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation.

What is the deductible?

The deductible is the annual amount you pay first before basic insurance contributes to costs. A higher deductible lowers the premium but increases your risk.

Low or high deductible?

A low deductible often fits if you expect regular treatment. A high deductible can fit if you expect few costs and have enough reserve.

- CHF 300: lower risk, higher premium

- CHF 2,500: lower premium, higher risk

- adults and children separately

- review every year

How the app helps

PrimAI connects your current policy with possible premiums and shows whether deductible, model or insurer is the better lever.

Read the deductible as an annual budget

The deductible should not be chosen by monthly premium alone. Look at the full year: premium, maximum deductible exposure, coinsurance, medication, expected treatment and available reserve. PrimAI makes this a concrete decision instead of a discount calculation.

Adults, children and family context

An adult deductible is not the same decision as a child deductible. In a family, each person may need a different combination. The app separates policies so one person’s choice is not blindly copied to another.

Guide

Choose Swiss health insurance deductible | PrimAI

Which deductible fits in Switzerland? PrimAI helps check risk, expected health costs and official premiums in the free app.

What is the deductible?

The deductible is the annual amount you pay first before basic insurance contributes to costs. A higher deductible lowers the premium but increases your risk.

Low or high deductible?

A low deductible often fits if you expect regular treatment. A high deductible can fit if you expect few costs and have enough reserve.

How the app helps

PrimAI connects your current policy with possible premiums and shows whether deductible, model or insurer is the better lever.

Read the deductible as an annual budget

The deductible should not be chosen by monthly premium alone. Look at the full year: premium, maximum deductible exposure, coinsurance, medication, expected treatment and available reserve. PrimAI makes this a concrete decision instead of a discount calculation.

Which deductible fits in Switzerland? PrimAI helps check risk, expected health costs and official premiums in the free app.

The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation.

Guide, app and insurer compared

Guide

Which deductible fits in Switzerland? PrimAI helps check risk, expected health costs and official premiums in the free app.

PrimAI App

The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation.

Health insurer

Official confirmation, contract handling and administration.

| Level | What it is good for | Best for |

|---|---|---|

| Guide | Which deductible fits in Switzerland? PrimAI helps check risk, expected health costs and official premiums in the free app. | Understanding the topic before acting. |

| PrimAI App | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. | Preparing the concrete task on your phone. |

| Health insurer | Official confirmation, contract handling and administration. | Legally binding confirmation. |

What is the deductible?: The deductible is the annual amount you pay first before basic insurance contributes to costs. A higher deductible lowers the premium but increases your risk.

Low or high deductible?: A low deductible often fits if you expect regular treatment. A high deductible can fit if you expect few costs and have enough reserve. CHF 300: lower risk, higher premium CHF 2,500: lower premium, higher risk adults and children separately review every year

How the app helps: PrimAI connects your current policy with possible premiums and shows whether deductible, model or insurer is the better lever.

Read the deductible as an annual budget: The deductible should not be chosen by monthly premium alone. Look at the full year: premium, maximum deductible exposure, coinsurance, medication, expected treatment and available reserve. PrimAI makes this a concrete decision instead of a discount calculation.

Adults, children and family context: An adult deductible is not the same decision as a child deductible. In a family, each person may need a different combination. The app separates policies so one person’s choice is not blindly copied to another.

Check deductible in the app

Can I change deductible every year? Yes, generally if deadlines are met.

Is the highest deductible always cheapest? Not always. It lowers the premium, but increases risk when health costs appear.

Can PrimAI prepare the request? Yes, the app can help prepare documents for a change.

Which deductible fits regular medical costs? A low deductible is often more cautious with regular costs, but the full annual burden should be compared.

Checklist for Deductible

| Point | Why it matters | How PrimAI helps |

|---|---|---|

| What is the deductible? | The deductible is the annual amount you pay first before basic insurance contributes to costs. A higher deductible lowers the premium but increases your risk. | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. |

| Low or high deductible? | A low deductible often fits if you expect regular treatment. A high deductible can fit if you expect few costs and have enough reserve. | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. |

| How the app helps | PrimAI connects your current policy with possible premiums and shows whether deductible, model or insurer is the better lever. | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. |

| Read the deductible as an annual budget | The deductible should not be chosen by monthly premium alone. Look at the full year: premium, maximum deductible exposure, coinsurance, medication, expected treatment and available reserve. PrimAI makes this a concrete decision instead of a discount calculation. | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. |

| Adults, children and family context | An adult deductible is not the same decision as a child deductible. In a family, each person may need a different combination. The app separates policies so one person’s choice is not blindly copied to another. | The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation. |

Check deductible in the app

The deductible is one of the most important levers. PrimAI helps compare low and high deductible options with your real situation.

Download the app for free →

Free app for Switzerland

On desktop? Scan the code with your phone.

The best flow is on mobile: scan the QR code, open the app and continue with your policy there.

FAQ

Frequently asked questions

Can I change deductible every year?

Yes, generally if deadlines are met.

Is the highest deductible always cheapest?

Not always. It lowers the premium, but increases risk when health costs appear.

Can PrimAI prepare the request?

Yes, the app can help prepare documents for a change.

Which deductible fits regular medical costs?

A low deductible is often more cautious with regular costs, but the full annual burden should be compared.