Models

The model has to fit your daily life.

HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes.

- ✓Family doctor

- ✓HMO

- ✓Telmed

- ✓Standard

Standard, family doctor, HMO or Telmed: PrimAI explains health insurance models and helps check the right model in the app.

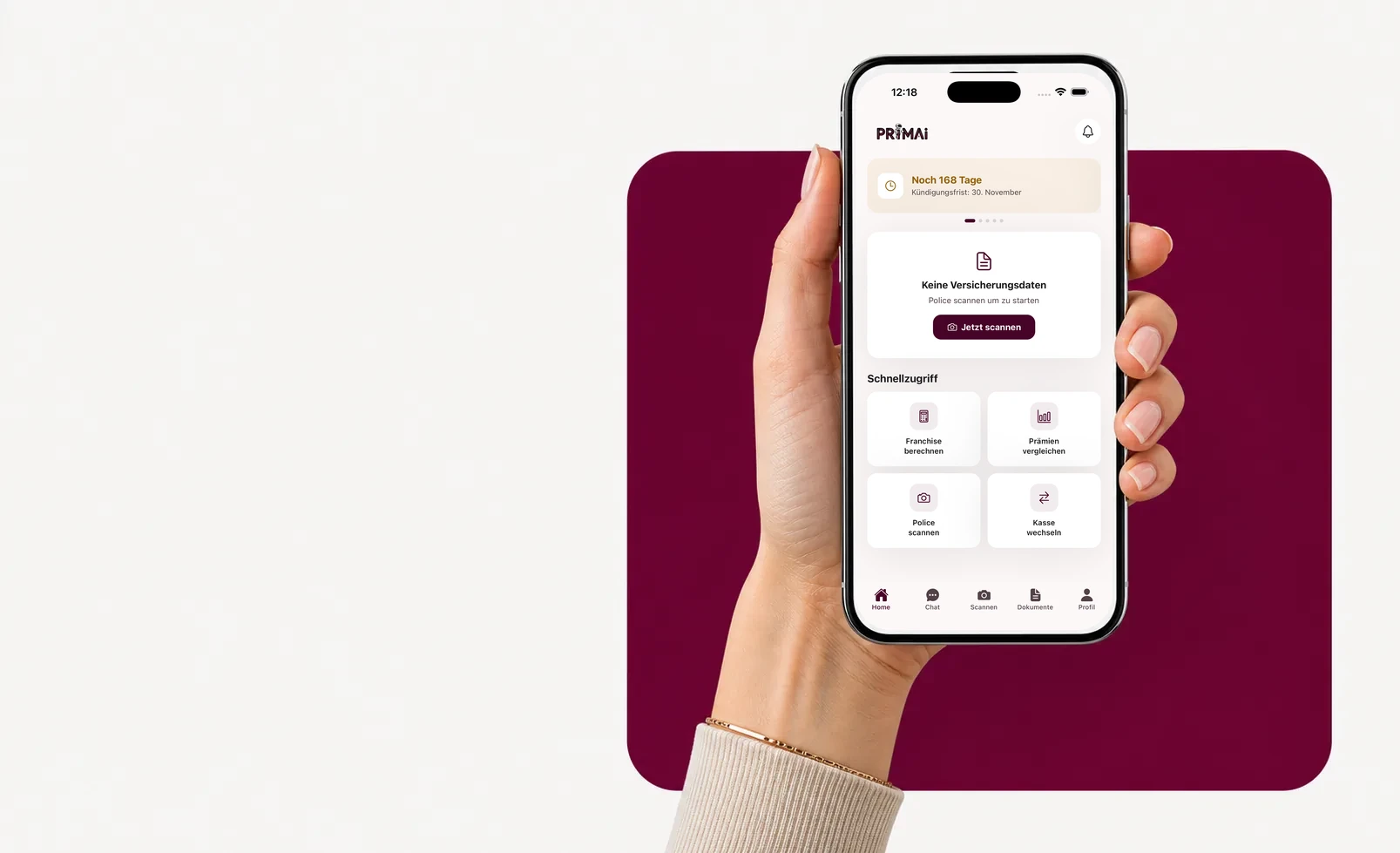

PrimAI app

Turn your policy into a clear app task.

Scan your policy, check official FOPH premiums, keep the deadline in view and prepare the right document — neutral, free and without commission.

Guide

Which models exist?

HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes.

Which models exist?

The standard model usually offers more freedom. Family doctor, HMO and Telmed define a first point of contact before certain treatments.

- Standard: more freedom, often higher premium

- family doctor: fixed first contact

- HMO: group practice coordination

- Telmed: first contact by phone or digital channel

Why models can save money

Alternative models can reduce premiums because they coordinate access to care. The model still has to match your real behaviour.

How PrimAI helps with model changes

The app helps identify your current model, understand alternatives and prepare a change.

The model should match your first instinct

If you already call your family doctor first, a family doctor model can feel natural. If you want broad choice, standard may still fit despite the higher premium. PrimAI connects real behaviour with price.

Different product names, similar logic

Insurers use different product names. Behind those names are often the same principles: family doctor, HMO, Telmed or standard access. The app translates the policy name into a rule you can understand.

Guide

Swiss health insurance models: HMO, family doctor, Telmed | PrimAI

Standard, family doctor, HMO or Telmed: PrimAI explains health insurance models and helps check the right model in the app.

Which models exist?

The standard model usually offers more freedom. Family doctor, HMO and Telmed define a first point of contact before certain treatments.

Why models can save money

Alternative models can reduce premiums because they coordinate access to care. The model still has to match your real behaviour.

How PrimAI helps with model changes

The app helps identify your current model, understand alternatives and prepare a change.

The model should match your first instinct

If you already call your family doctor first, a family doctor model can feel natural. If you want broad choice, standard may still fit despite the higher premium. PrimAI connects real behaviour with price.

Standard, family doctor, HMO or Telmed: PrimAI explains health insurance models and helps check the right model in the app.

HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes.

Guide, app and insurer compared

Guide

Standard, family doctor, HMO or Telmed: PrimAI explains health insurance models and helps check the right model in the app.

PrimAI App

HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes.

Health insurer

Official confirmation, contract handling and administration.

| Level | What it is good for | Best for |

|---|---|---|

| Guide | Standard, family doctor, HMO or Telmed: PrimAI explains health insurance models and helps check the right model in the app. | Understanding the topic before acting. |

| PrimAI App | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. | Preparing the concrete task on your phone. |

| Health insurer | Official confirmation, contract handling and administration. | Legally binding confirmation. |

Which models exist?: The standard model usually offers more freedom. Family doctor, HMO and Telmed define a first point of contact before certain treatments. Standard: more freedom, often higher premium family doctor: fixed first contact HMO: group practice coordination Telmed: first contact by phone or digital channel

Why models can save money: Alternative models can reduce premiums because they coordinate access to care. The model still has to match your real behaviour.

How PrimAI helps with model changes: The app helps identify your current model, understand alternatives and prepare a change.

The model should match your first instinct: If you already call your family doctor first, a family doctor model can feel natural. If you want broad choice, standard may still fit despite the higher premium. PrimAI connects real behaviour with price.

Different product names, similar logic: Insurers use different product names. Behind those names are often the same principles: family doctor, HMO, Telmed or standard access. The app translates the policy name into a rule you can understand.

Check model in the app

Are benefits worse in HMO or Telmed? No. Legal basic benefits are the same. Access rules change.

Can I change model every year? Generally yes, if the change is requested on time.

Which model is best? It depends on your daily life, flexibility needs and medical habits.

Does a cheaper model limit freedom? Often yes, at least for the first medical contact. That is exactly the rule to understand before choosing.

Checklist for Models

| Point | Why it matters | How PrimAI helps |

|---|---|---|

| Which models exist? | The standard model usually offers more freedom. Family doctor, HMO and Telmed define a first point of contact before certain treatments. | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. |

| Why models can save money | Alternative models can reduce premiums because they coordinate access to care. The model still has to match your real behaviour. | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. |

| How PrimAI helps with model changes | The app helps identify your current model, understand alternatives and prepare a change. | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. |

| The model should match your first instinct | If you already call your family doctor first, a family doctor model can feel natural. If you want broad choice, standard may still fit despite the higher premium. PrimAI connects real behaviour with price. | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. |

| Different product names, similar logic | Insurers use different product names. Behind those names are often the same principles: family doctor, HMO, Telmed or standard access. The app translates the policy name into a rule you can understand. | HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes. |

Check model in the app

HMO, family doctor, Telmed or standard: basic benefits are the same, but access to care changes.

Download the app for free →

Free app for Switzerland

On desktop? Scan the code with your phone.

The best flow is on mobile: scan the QR code, open the app and continue with your policy there.

FAQ

Frequently asked questions

Are benefits worse in HMO or Telmed?

No. Legal basic benefits are the same. Access rules change.

Can I change model every year?

Generally yes, if the change is requested on time.

Which model is best?

It depends on your daily life, flexibility needs and medical habits.

Does a cheaper model limit freedom?

Often yes, at least for the first medical contact. That is exactly the rule to understand before choosing.