Dental Insurance

Prepare dental costs before they become a surprise.

Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions.

- ✓Children and orthodontics

- ✓Estimates and invoices

- ✓Separate cover

Understand Swiss dental insurance: dental costs, children, orthodontics, basic insurance, supplemental cover and documents in the PrimAI app.

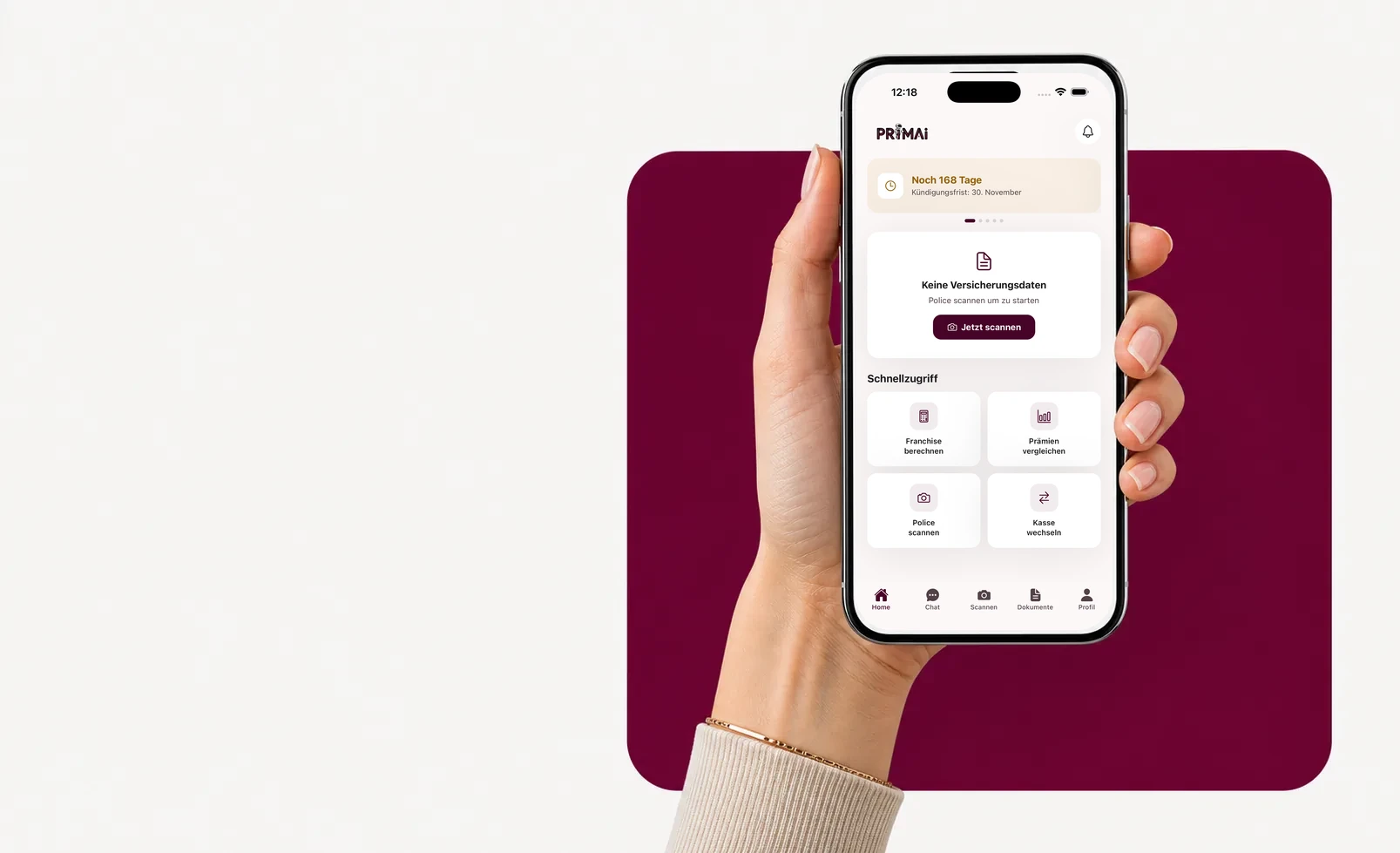

PrimAI app

Turn your policy into a clear app task.

Scan your policy, check official FOPH premiums, keep the deadline in view and prepare the right document — neutral, free and without commission.

Guide

What basic insurance usually does not pay

Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions.

What basic insurance usually does not pay

In Switzerland, ordinary dental treatment is usually paid by the insured person. Exceptions can exist for serious illness, accidents or specific medical situations, but routine dental care should not be assumed to be reimbursed automatically.

Children and orthodontics

For children, dental insurance often becomes important when orthodontics appears. Dental cover can help, but conditions, waiting periods and timing matter. A policy arranged early is different from a new application after a large treatment plan already exists.

- child age

- orthodontic estimate

- waiting period

- yearly limit

- acceptance rules

Insurance or savings budget?

Dental insurance is not automatically better than setting money aside. Compare yearly premium, expected reimbursements, limits, likely treatments and exclusions. PrimAI helps collect the documents that make this comparison real: estimates, invoices, insurer answers and current policy.

Documents to keep

Treatment plans, dentist estimates, invoices, receipts, reimbursement decisions and policy conditions should stay together. Otherwise it becomes difficult to understand whether the cover was useful or why a claim was rejected.

What the app adds

PrimAI does not sell dental insurance. The app helps you create a task: check the policy, attach an estimate, note the question for the insurer, keep the answer and prepare the next step without losing context.

Personal advice

Want your dental cover reviewed?

Limits, waiting periods and health questions make dental cover tricky. For English-speaking advice, we recommend Expat Savvy.

Guide

Dental Insurance Switzerland | PrimAI

Understand Swiss dental insurance: dental costs, children, orthodontics, basic insurance, supplemental cover and documents in the PrimAI app.

What basic insurance usually does not pay

In Switzerland, ordinary dental treatment is usually paid by the insured person. Exceptions can exist for serious illness, accidents or specific medical situations, but routine dental care should not be assumed to be reimbursed automatically.

Children and orthodontics

For children, dental insurance often becomes important when orthodontics appears. Dental cover can help, but conditions, waiting periods and timing matter. A policy arranged early is different from a new application after a large treatment plan already exists.

Insurance or savings budget?

Dental insurance is not automatically better than setting money aside. Compare yearly premium, expected reimbursements, limits, likely treatments and exclusions. PrimAI helps collect the documents that make this comparison real: estimates, invoices, insurer answers and current policy.

Documents to keep

Treatment plans, dentist estimates, invoices, receipts, reimbursement decisions and policy conditions should stay together. Otherwise it becomes difficult to understand whether the cover was useful or why a claim was rejected.

Understand Swiss dental insurance: dental costs, children, orthodontics, basic insurance, supplemental cover and documents in the PrimAI app.

Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions.

Guide, app and insurer compared

Guide

Understand Swiss dental insurance: dental costs, children, orthodontics, basic insurance, supplemental cover and documents in the PrimAI app.

PrimAI App

Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions.

Health insurer

Official confirmation, contract handling and administration.

| Level | What it is good for | Best for |

|---|---|---|

| Guide | Understand Swiss dental insurance: dental costs, children, orthodontics, basic insurance, supplemental cover and documents in the PrimAI app. | Understanding the topic before acting. |

| PrimAI App | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. | Preparing the concrete task on your phone. |

| Health insurer | Official confirmation, contract handling and administration. | Legally binding confirmation. |

What basic insurance usually does not pay: In Switzerland, ordinary dental treatment is usually paid by the insured person. Exceptions can exist for serious illness, accidents or specific medical situations, but routine dental care should not be assumed to be reimbursed automatically.

Children and orthodontics: For children, dental insurance often becomes important when orthodontics appears. Dental cover can help, but conditions, waiting periods and timing matter. A policy arranged early is different from a new application after a large treatment plan already exists. child age orthodontic estimate waiting period yearly limit acceptance rules

Insurance or savings budget?: Dental insurance is not automatically better than setting money aside. Compare yearly premium, expected reimbursements, limits, likely treatments and exclusions. PrimAI helps collect the documents that make this comparison real: estimates, invoices, insurer answers and current policy.

Documents to keep: Treatment plans, dentist estimates, invoices, receipts, reimbursement decisions and policy conditions should stay together. Otherwise it becomes difficult to understand whether the cover was useful or why a claim was rejected.

What the app adds: PrimAI does not sell dental insurance. The app helps you create a task: check the policy, attach an estimate, note the question for the insurer, keep the answer and prepare the next step without losing context.

Organise dental documents

Does basic insurance pay dental costs? Usually not, except for specific cases such as certain illnesses or accidents.

When should I check dental cover for a child? Ideally before major treatment is already planned.

Does PrimAI guarantee reimbursement? No. PrimAI organises documents and questions; the insurer decides.

Checklist for Dental Insurance

| Point | Why it matters | How PrimAI helps |

|---|---|---|

| What basic insurance usually does not pay | In Switzerland, ordinary dental treatment is usually paid by the insured person. Exceptions can exist for serious illness, accidents or specific medical situations, but routine dental care should not be assumed to be reimbursed automatically. | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. |

| Children and orthodontics | For children, dental insurance often becomes important when orthodontics appears. Dental cover can help, but conditions, waiting periods and timing matter. A policy arranged early is different from a new application after a large treatment plan already exists. | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. |

| Insurance or savings budget? | Dental insurance is not automatically better than setting money aside. Compare yearly premium, expected reimbursements, limits, likely treatments and exclusions. PrimAI helps collect the documents that make this comparison real: estimates, invoices, insurer answers and current policy. | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. |

| Documents to keep | Treatment plans, dentist estimates, invoices, receipts, reimbursement decisions and policy conditions should stay together. Otherwise it becomes difficult to understand whether the cover was useful or why a claim was rejected. | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. |

| What the app adds | PrimAI does not sell dental insurance. The app helps you create a task: check the policy, attach an estimate, note the question for the insurer, keep the answer and prepare the next step without losing context. | Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions. |

Organise dental documents

Dental care is often covered less than people expect in Switzerland. PrimAI helps organise policy, estimates, invoices and insurer questions.

Download the app for free →

Free app for Switzerland

On desktop? Scan the code with your phone.

The best flow is on mobile: scan the QR code, open the app and continue with your policy there.

FAQ

Frequently asked questions

Does basic insurance pay dental costs?

Usually not, except for specific cases such as certain illnesses or accidents.

When should I check dental cover for a child?

Ideally before major treatment is already planned.

Does PrimAI guarantee reimbursement?

No. PrimAI organises documents and questions; the insurer decides.