Switching

Switch from SWICA: swica: health topics, model and documents kept apart before cancellation.

PrimAI helps check your SWICA policy, compare official FOPH premiums, test deductible and model, then prepare only the useful documents in the app. PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

- ✓Official premiums

- ✓Current policy

- ✓Neutral decision

Switch from SWICA: compare official premiums, check deductible and model, then prepare documents in the PrimAI app without commission.

Quick facts

Switching: the essentials at a glance.

Step by step

How it works.

-

Compare official premiums

Compare FOPH premiums for your address before switching.

-

Check model and deductible

Pick from SWICA models and the right deductible.

-

Choose the new insurer

Only cancel once the new basic insurance fits.

-

Prepare the cancellation

PrimAI coordinates cancellation and the start of the new policy.

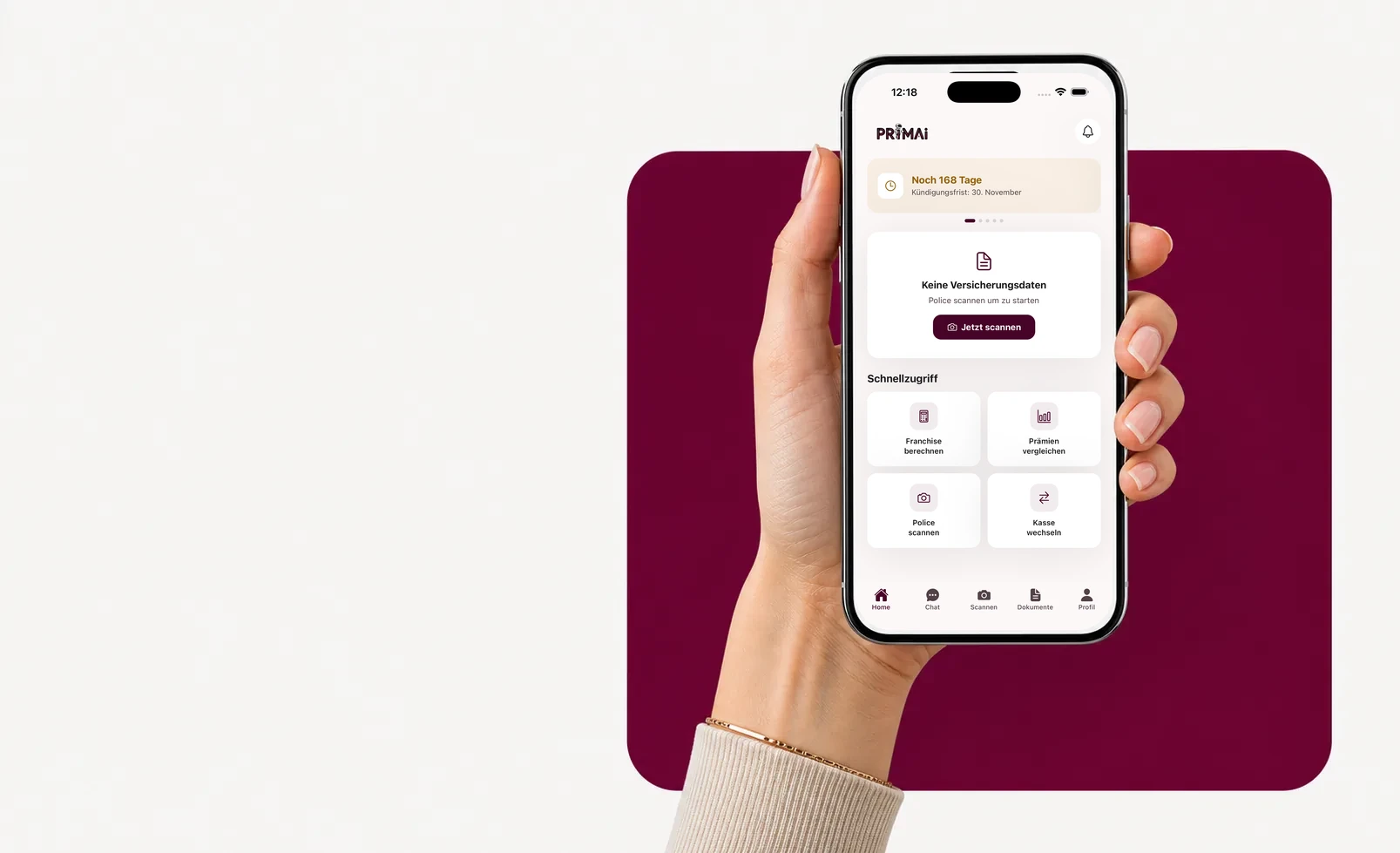

PrimAI app

Turn your policy into a clear app task.

Scan your policy, check official FOPH premiums, keep the deadline in view and prepare the right document — neutral, free and without commission.

Models

Switching basic-insurance models.

The model sets premium and doctor access. Swipe through the options.

Standard (freie Arztwahl)

Basic benefits are the same by law — models differ in access and premium.

Medica

Basic benefits are the same by law — models differ in access and premium.

Casa

Basic benefits are the same by law — models differ in access and premium.

Medpharm

Basic benefits are the same by law — models differ in access and premium.

Favorit Santé

Basic benefits are the same by law — models differ in access and premium.

Telmed

Basic benefits are the same by law — models differ in access and premium.

Step by step

Why switching depends on your current policy

PrimAI helps check your SWICA policy, compare official FOPH premiums, test deductible and model, then prepare only the useful documents in the app. PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

Why switching depends on your current policy

SWICA can combine basic insurance, alternative models and supplementary health topics. PrimAI helps read them separately. PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

- Clear model

- Separate supplementary cover

- Neutral

Premium comparison is not enough

A switch from SWICA should not start from one monthly amount. Basic insurance benefits are defined by law, but the premium depends on residence, premium region, deductible, insurance model, age and accident cover. PrimAI puts comparison back into that context: current policy, official premiums and the parameters that actually change the annual cost.

Optimize before leaving

Before leaving SWICA, it is worth checking whether internal optimization is enough: another deductible, family doctor model, HMO, Telmed, accident cover or an address correction. This avoids preparing cancellation when a smaller change already solves the issue. PrimAI presents those options as separate tasks, not as pressure to switch.

The new insurer has to be ready

Switching also means choosing a new starting point with another insurer. The new option must match your residence, preferred model, deductible risk and timing. PrimAI helps keep that new situation visible before touching the SWICA cancellation step, so you do not leave a known policy without an understandable alternative.

What changes by current insurer

PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

- Clear model

- Separate supplementary cover

- Neutral

Cancellation comes after the decision

SWICA cancellation comes only when the decision is clear. For basic insurance, the late-November deadline is often central; for supplementary insurance, different contract rules can apply. PrimAI separates comparison, optimization and cancellation so the document contains only the correct and necessary data. Before changing insurer, it may be useful to check deductible, model and official premiums. PrimAI prepares this comparison using your current policy as the starting point.

Guide

SWICA: switching with swica: health topics, model and documents kept apart | PrimAI

Switch from SWICA: compare official premiums, check deductible and model, then prepare documents in the PrimAI app without commission.

Guide, app and insurer compared

Guide

Switch from SWICA: compare official premiums, check deductible and model, then prepare documents in the PrimAI app without commission.

Best for: Understanding the topic before acting.

PrimAI App

PrimAI helps check your SWICA policy, compare official FOPH premiums, test deductible and model, then prepare only the useful documents in the app. PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

Best for: Preparing the concrete task on your phone.

Health insurer

Official confirmation, contract handling and administration.

Best for: Legally binding confirmation.

Download the free app

PrimAI helps check your SWICA policy, compare official FOPH premiums, test deductible and model, then prepare only the useful documents in the app. PrimAI does not give medical advice and does not sell insurance. The app organizes information, prepares documents and keeps neutrality visible.

Download the app for free →

Free app for Switzerland

On desktop? Scan the code with your phone.

The best flow is on mobile: scan the QR code, open the app and continue with your policy there.

FAQ

Frequently asked questions

Where do I send the SWICA basic-insurance cancellation?

To: SWICA Krankenversicherung AG, Römerstrasse 38, 8401 Winterthur. It must arrive by 30 November (date of receipt, not postmark).

Which models does SWICA offer?

SWICA offers: Standard (freie Arztwahl), Medica, Casa, Medpharm, Favorit Santé, Telmed. The model affects premium and doctor access.

How do I reach SWICA?

Via the mySWICA portal or by phone at 0800 80 90 80.

Does PrimAI sell an alternative to SWICA?

No. PrimAI does not sell health insurance and receives no commission.

Should I cancel SWICA before choosing a new insurer?

No. For basic insurance, the new situation should be clear before cancellation is sent.

Why does the deductible matter so much?

It changes annual risk. A low premium with a high deductible can be a bad fit when health costs are regular.

Does PrimAI use official premiums?

The app positioning is to work from your current policy and official premiums as a neutral basis.